import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from statsmodels.graphics.tsaplots import acf as acf_func

plt.style.use("ggplot")

import arch

import yfinance as yf

import datetime as dt

from statsmodels.tsa.arima.model import ARIMAWe need to model volatility for risk management and trading.

ARCH and GARCH

Conditional Heteroskedasticity is the academic term for volatility clustering. \(\text{ARCH}(1)\) formulation is

\[ \epsilon_t= \sigma_t w_t \] where \(\{w_t\}\) is a white noise process.

\[ \sigma_t^2=\alpha_0 + \alpha_1 \epsilon_{t-1}^2 \] \(\{\epsilon_t\}\) is autoregressive conditional heteroskedastic process with order unity.

A slight modification will show that how \(\text{ARCH}\) models volatility \[\begin{aligned} \operatorname{Var}\left(\epsilon_t\right) & =\mathrm{E}\left[\epsilon_t^2\right]-\left(\mathrm{E}\left[\epsilon_t\right]\right)^2 \\ & =\mathrm{E}\left[\epsilon_t^2\right] \\ & =\mathrm{E}\left[w_t^2\right] \mathrm{E}\left[\alpha_0+\alpha_1 \epsilon_{t-1}^2\right] \\ & =\mathrm{E}\left[\alpha_0+\alpha_1 \epsilon_{t-1}^2\right] \\ & =\alpha_0+\alpha_1 \operatorname{Var}\left(\epsilon_{t-1}\right) \end{aligned}\]Simply put \[ \operatorname{Var}=\alpha_0+\alpha_1 \operatorname{Var}\left(\epsilon_{t-1}\right) \] which is also an \(\text{AR}(1)\).

For \(\text{AR}(p)\) \[ \epsilon_t=w_t \sqrt{\alpha_0+\sum_{i=1}^p \alpha_p \epsilon_{t-i}^2} \]

The counterpart of \(\text{ARMA}\) is Generalised Autoregressive Conditional Heteroskedastic (\(\text{GARCH}\)), usually formulated as \[ \begin{align} \epsilon_t&= \sigma_t w_t\\ \sigma_t^2&=\alpha_0+\sum_{i=1}^q \alpha_i \epsilon_{t-i}^2+\sum_{j=1}^p \beta_j \sigma_{t-j}^2 \end{align} \] We say \(\{\epsilon_t\}\) is a \(\text{GARCH}(p, q)\) process.

GARCH(1, 1) Simulation

\[\begin{aligned} \epsilon_t & =\sigma_t w_t \\ \sigma_t^2 & =\alpha_0+\alpha_1 \epsilon_{t-1}^2+\beta_1 \sigma_{t-1}^2 \end{aligned}\]If \(\alpha_1+\beta_1<1\), the system is stable, otherwise unstable.

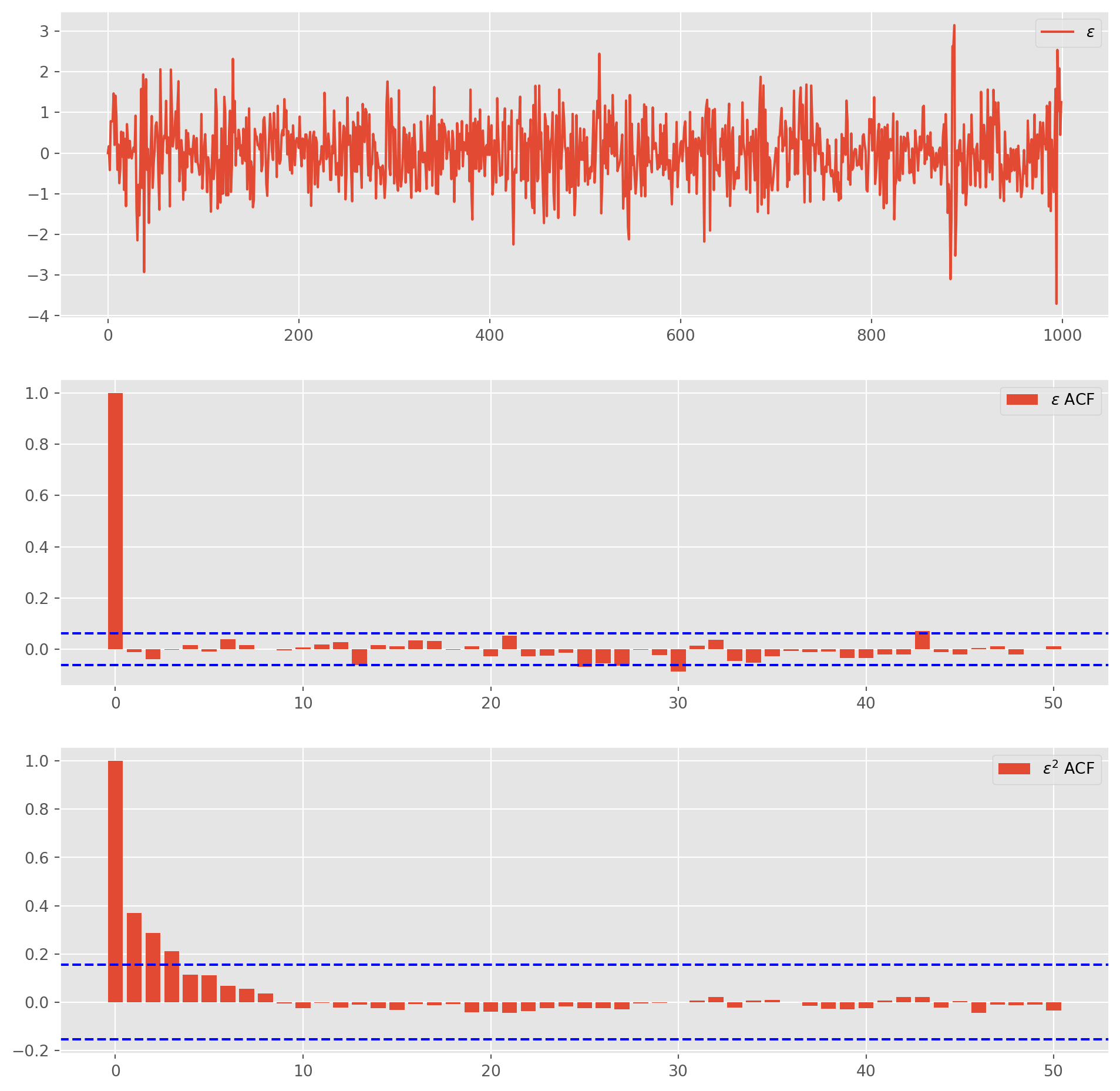

Generate \(\text{GARCH}(1, 1)\) data.

def gen_garch11(a0, a1, b1, N):

w = np.random.randn(N)

epsilon = np.zeros(N)

sigma_sq = np.zeros(N)

for i in range(1, N):

sigma_sq[i] = a0 + a1 * epsilon[i - 1] ** 2 + b1 * sigma_sq[i - 1]

epsilon[i] = w[i] * np.sqrt(sigma_sq[i])

return epsilonepsilon = gen_garch11(a0=0.2, a1=0.3, b1=0.4, N=1000)Plot generated data and ACFs.

epsilon_acf = acf_func(epsilon, nlags=50)

epsilon_acf_sq = acf_func(epsilon**2, nlags=50)fig, ax = plt.subplots(figsize=(12, 12), nrows=3, ncols=1)

ax[0].plot(epsilon, label="$\epsilon$")

ax[1].bar(np.arange(len(epsilon_acf)), epsilon_acf, label="$\epsilon$ ACF")

ax[1].axhline(np.std(epsilon_acf[1:]) * 1.96, ls="--", color="b")

ax[1].axhline(-np.std(epsilon_acf[1:]) * 1.96, ls="--", color="b")

ax[2].bar(np.arange(len(epsilon_acf)), epsilon_acf_sq, label="$\epsilon^2$ ACF")

ax[2].axhline(np.std(epsilon_acf_sq[1:]) * 1.96, ls="--", color="b")

ax[2].axhline(-np.std(epsilon_acf_sq[1:]) * 1.96, ls="--", color="b")

for i in range(3):

ax[i].legend()

plt.show()<>:2: SyntaxWarning:

invalid escape sequence '\e'

<>:4: SyntaxWarning:

invalid escape sequence '\e'

<>:8: SyntaxWarning:

invalid escape sequence '\e'

<>:2: SyntaxWarning:

invalid escape sequence '\e'

<>:4: SyntaxWarning:

invalid escape sequence '\e'

<>:8: SyntaxWarning:

invalid escape sequence '\e'

/tmp/ipykernel_4645/683653153.py:2: SyntaxWarning:

invalid escape sequence '\e'

/tmp/ipykernel_4645/683653153.py:4: SyntaxWarning:

invalid escape sequence '\e'

/tmp/ipykernel_4645/683653153.py:8: SyntaxWarning:

invalid escape sequence '\e'

Note that \(\epsilon\) looks like white noise, in contrast \(\epsilon^2\) shows autocorrelation and volatility clustering.

model = arch.arch_model(epsilon, mean="Zero", vol="GARCH", p=1, o=0, q=1)

res = model.fit()Iteration: 1, Func. Count: 5, Neg. LLF: 827535.1835085036

Iteration: 2, Func. Count: 10, Neg. LLF: 1151.346750915227

Iteration: 3, Func. Count: 15, Neg. LLF: 1150.5779430693185

Iteration: 4, Func. Count: 21, Neg. LLF: 1175.1702226992597

Iteration: 5, Func. Count: 26, Neg. LLF: 1112.519073761109

Iteration: 6, Func. Count: 30, Neg. LLF: 1112.5190355232094

Iteration: 7, Func. Count: 34, Neg. LLF: 1112.519033642905

Iteration: 8, Func. Count: 37, Neg. LLF: 1112.519033642824

Optimization terminated successfully (Exit mode 0)

Current function value: 1112.519033642905

Iterations: 8

Function evaluations: 37

Gradient evaluations: 8print(res.summary()) Zero Mean - GARCH Model Results

==============================================================================

Dep. Variable: y R-squared: 0.000

Mean Model: Zero Mean Adj. R-squared: 0.001

Vol Model: GARCH Log-Likelihood: -1112.52

Distribution: Normal AIC: 2231.04

Method: Maximum Likelihood BIC: 2245.76

No. Observations: 1000

Date: Sun, Oct 27 2024 Df Residuals: 1000

Time: 17:40:33 Df Model: 0

Volatility Model

==========================================================================

coef std err t P>|t| 95.0% Conf. Int.

--------------------------------------------------------------------------

omega 0.1455 4.705e-02 3.093 1.984e-03 [5.330e-02, 0.238]

alpha[1] 0.2516 5.495e-02 4.578 4.684e-06 [ 0.144, 0.359]

beta[1] 0.5074 0.112 4.520 6.191e-06 [ 0.287, 0.727]

==========================================================================

Covariance estimator: robustCompare estimated coefficients with our preset true value.

res.paramsomega 0.145524

alpha[1] 0.251595

beta[1] 0.507414

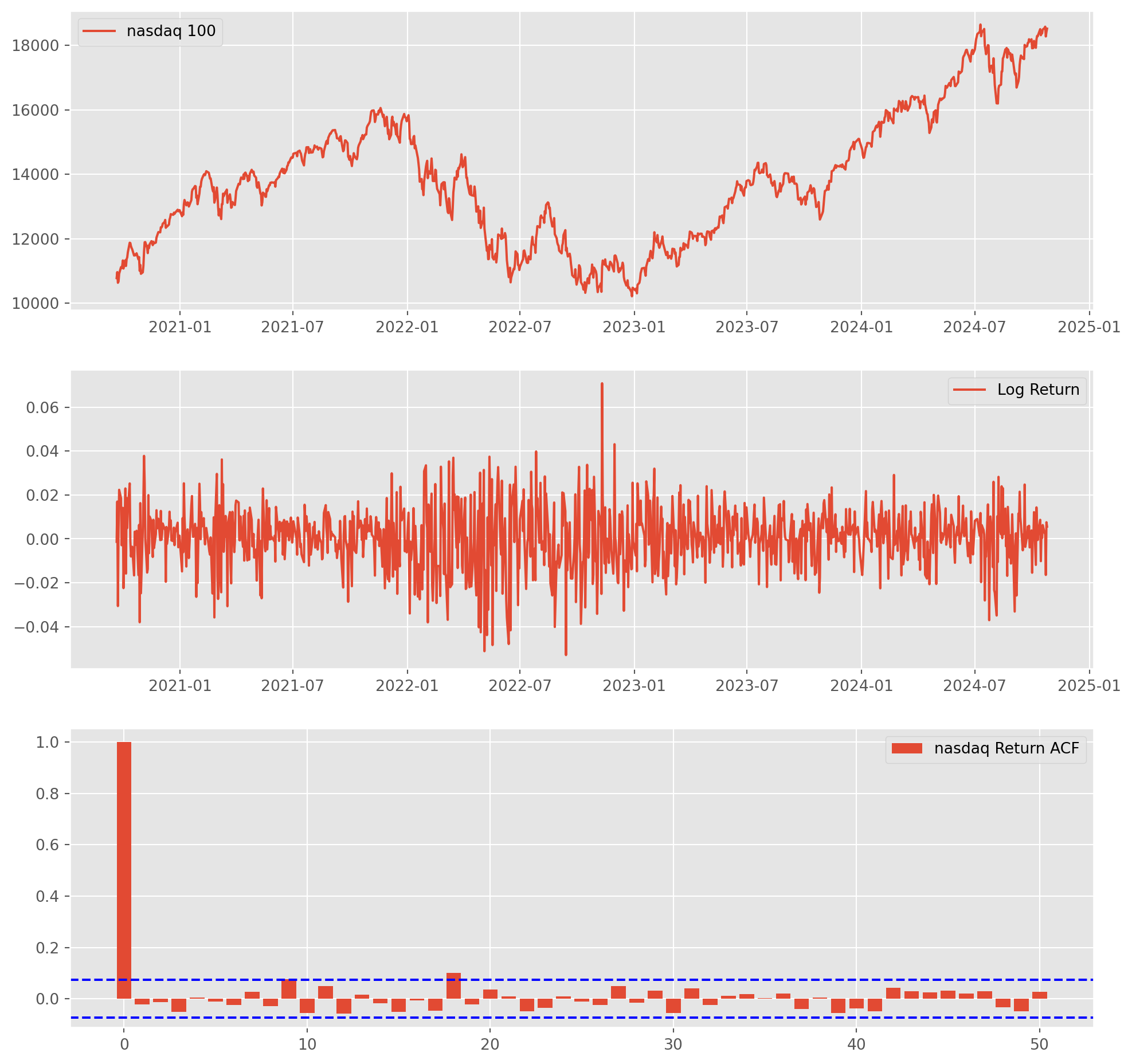

Name: params, dtype: float64Fitting Nasdaq Data

nasdaq = yf.download(

["^IXIC"],

start=dt.datetime.today() - dt.timedelta(days=1500),

end=dt.datetime.today(),

progress=True,

actions="inline",

interval="1d",

)[*********************100%***********************] 1 of 1 completednasdaq["log_ret"] = np.log(nasdaq["Adj Close"]) - np.log(nasdaq["Adj Close"].shift())

nasdaq = nasdaq.dropna()

nasdaq_acf = acf_func(nasdaq["log_ret"], nlags=50)fig, ax = plt.subplots(figsize=(12, 12), nrows=3, ncols=1)

ax[0].plot(nasdaq["Adj Close"], label="nasdaq 100")

ax[1].plot(nasdaq["log_ret"], label="Log Return")

ax[2].bar(np.arange(len(nasdaq_acf)), nasdaq_acf, label="nasdaq Return ACF")

ax[2].axhline(np.std(nasdaq_acf[1:]) * 1.96, ls="--", color="b")

ax[2].axhline(-np.std(nasdaq_acf[1:]) * 1.96, ls="--", color="b")

for i in range(3):

ax[i].legend()

plt.show()

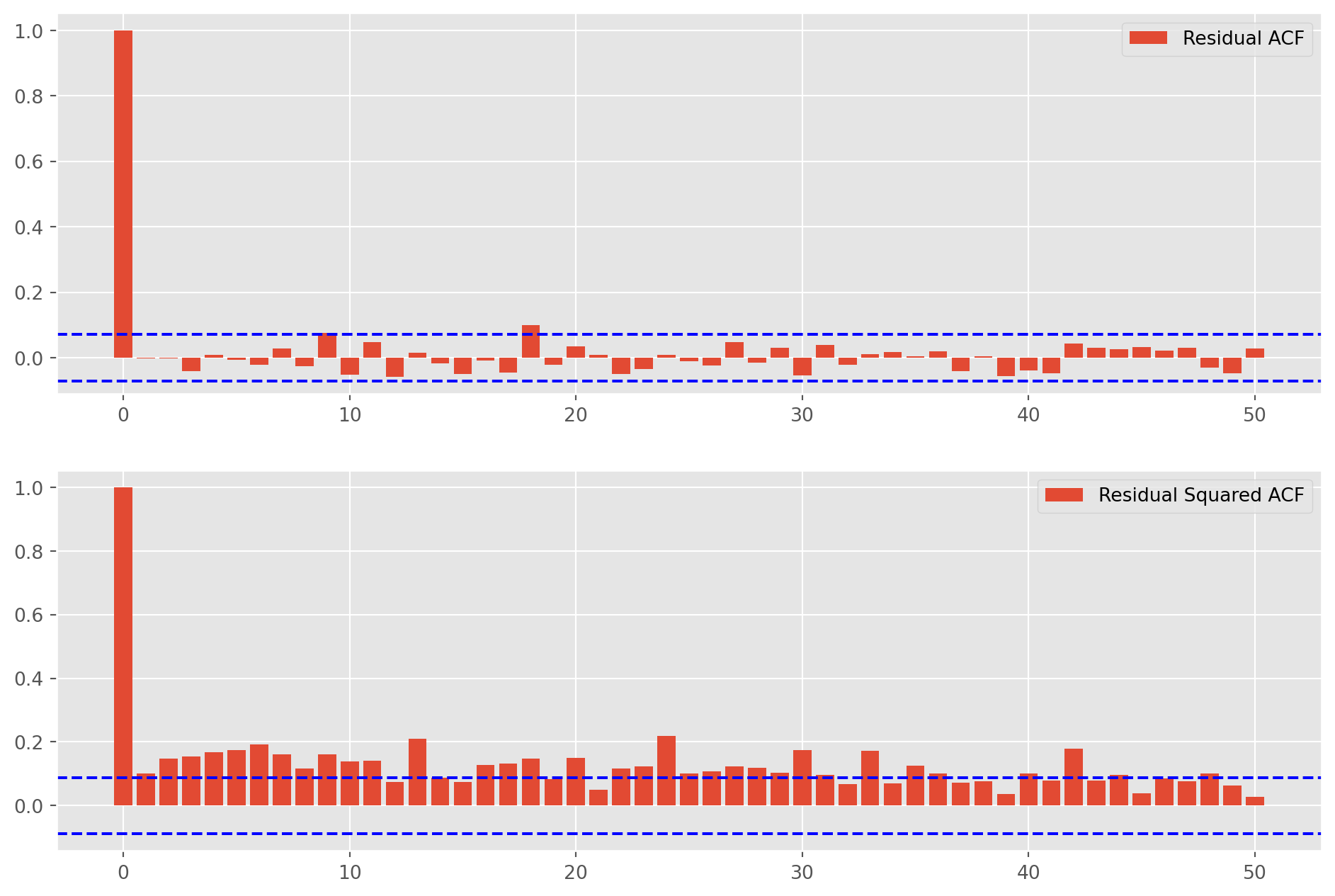

Fit the model with \(\text{ARIMA}\).

nasdaq.index = pd.DatetimeIndex(nasdaq.index).to_period(

"D"

) # without it, pandas will return warningmod_obj = ARIMA(nasdaq["log_ret"], order=(2, 0, 2))

results = mod_obj.fit()Now we want to see how much can’t \(\text{ARIMA}\) explain away in residual.

resid_acf = acf_func(results.resid, nlags=50)

resid_sq_acf = acf_func(results.resid**2, nlags=50)fig, ax = plt.subplots(figsize=(12, 8), nrows=2, ncols=1)

ax[0].bar(np.arange(len(resid_acf)), resid_acf, label="Residual ACF")

ax[0].axhline(np.std(resid_acf[1:]) * 1.96, ls="--", color="b")

ax[0].axhline(-np.std(resid_acf[1:]) * 1.96, ls="--", color="b")

ax[1].bar(np.arange(len(resid_sq_acf)), resid_sq_acf, label="Residual Squared ACF")

ax[1].axhline(np.std(resid_sq_acf[1:]) * 1.96, ls="--", color="b")

ax[1].axhline(-np.std(resid_sq_acf[1:]) * 1.96, ls="--", color="b")

for i in range(2):

ax[i].legend()

plt.show()

Auto correlation presents in the squared residuals, we are able to confirm conditional heteroskedastic behavior is present in the diff log return series of the Nasdaq.

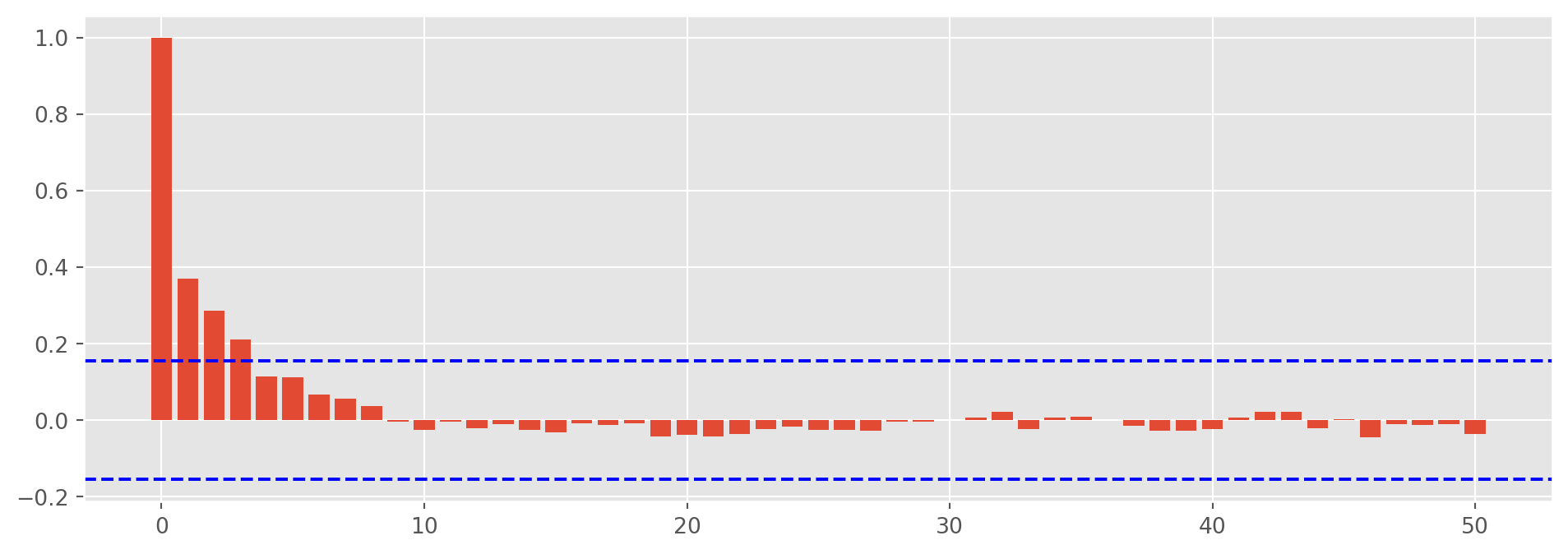

Therefore, we can fit a \(\text{GARCH}\) model. Note, we are fitting the log return, not the residuals of \(\text{ARIMA}\).

model_garch = arch.arch_model(

nasdaq["log_ret"], mean="Zero", vol="GARCH", p=1, o=0, q=1

)

res = model.fit()Iteration: 1, Func. Count: 5, Neg. LLF: 827535.1835085036

Iteration: 2, Func. Count: 10, Neg. LLF: 1151.346750915227

Iteration: 3, Func. Count: 15, Neg. LLF: 1150.5779430693185

Iteration: 4, Func. Count: 21, Neg. LLF: 1175.1702226992597

Iteration: 5, Func. Count: 26, Neg. LLF: 1112.519073761109

Iteration: 6, Func. Count: 30, Neg. LLF: 1112.5190355232094

Iteration: 7, Func. Count: 34, Neg. LLF: 1112.519033642905

Iteration: 8, Func. Count: 37, Neg. LLF: 1112.519033642824

Optimization terminated successfully (Exit mode 0)

Current function value: 1112.519033642905

Iterations: 8

Function evaluations: 37

Gradient evaluations: 8resid_garch_sq = res.resid**2resid_garch_sq_acf = acf_func(resid_garch_sq, nlags=50)fig, ax = plt.subplots(figsize=(12, 4))

ax.bar(np.arange(len(resid_garch_sq_acf)), resid_garch_sq_acf)

ax.axhline(np.std(resid_garch_sq_acf[1:]) * 1.96, ls="--", color="b")

ax.axhline(-np.std(resid_garch_sq_acf[1:]) * 1.96, ls="--", color="b")

plt.show()

The residuals still shows autocorrelation, it could mean that model is misspecified, we will investigate further later.